Futures Market: Overnight, LME copper opened at $9,539/mt, fluctuated upward throughout the session, bottomed at $9,510.5/mt during the fluctuations, peaked at $9,575/mt near the close, and finally settled at $9,558/mt, up 1.23%. Trading volume reached 18,000 lots, and open interest stood at 287,000 lots. Overnight, the most-traded SHFE copper 2504 contract opened higher at 77,940 yuan/mt, then the center shifted lower to bottom at 77,560 yuan/mt, followed by upward fluctuations, and finally closed at 77,670 yuan/mt, up 0.13%. Trading volume reached 20,000 lots, and open interest stood at 169,000 lots.

【SMM Copper Morning Brief】News: (1) US initial jobless claims for the week ending February 15 slightly exceeded expectations, recording 219,000, higher than the forecast of 215,000. The previous figure was revised from 213,000 to 214,000.

(2) The People's Bank of China: Implementing a moderately loose monetary policy, leveraging the dual functions of structural monetary policy tools in terms of total volume and structure, supporting technological innovation, and promoting consumption. Utilizing stock repurchase and refinancing tools to maintain stable capital market operations. Fully implementing the 25 measures to support private economy financing. Expanding private enterprise bond financing, strengthening risk-sharing mechanisms for private enterprise bonds, and supporting private enterprises in issuing sci-tech innovation bonds, green bonds, asset-backed securities, and other financing tools.

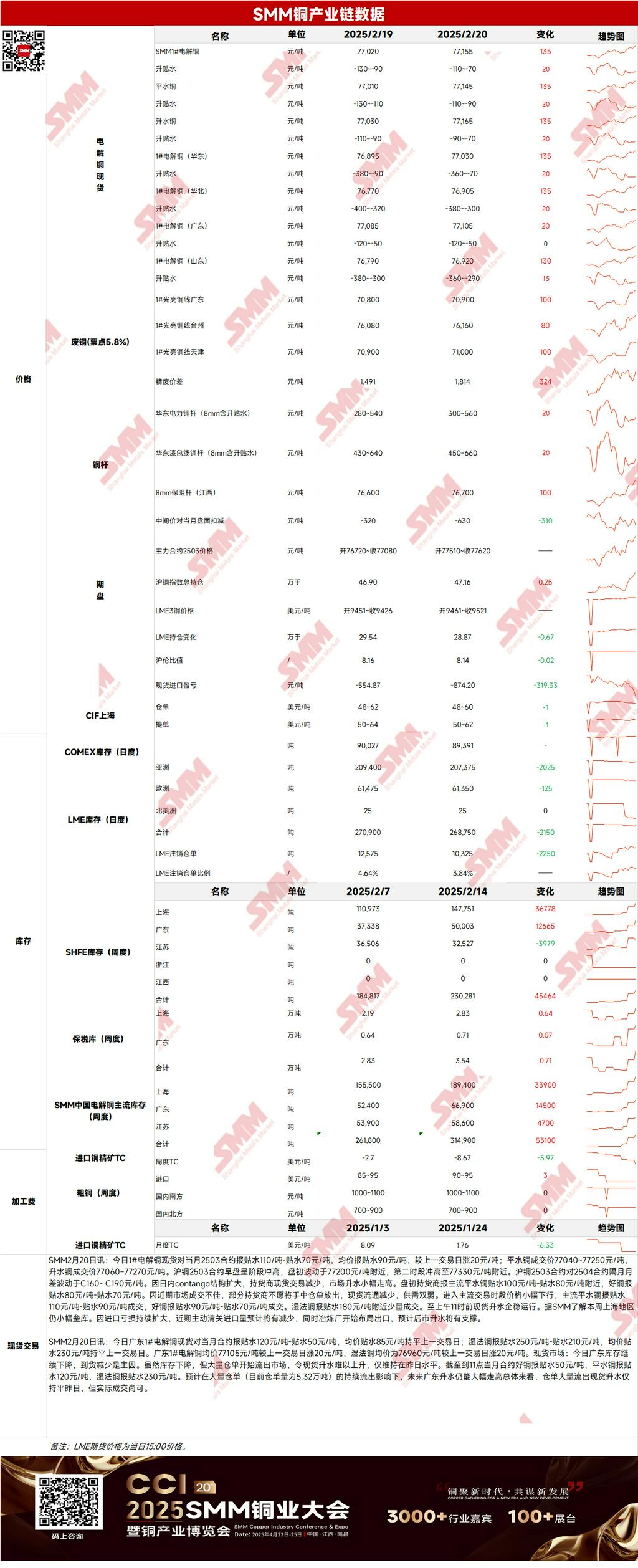

Spot Market: (1) Shanghai: On February 20, #1 copper cathode spot prices against the front-month 2503 contract were quoted at a discount of 110-70 yuan/mt, with an average discount of 90 yuan/mt, up 20 yuan/mt from the previous trading day. According to SMM, a slight inventory buildup continued in the Shanghai region this week. Due to the widening import losses, active customs clearance of imported copper is expected to decrease, while smelters have started planning for exports. Spot premiums are expected to gain support in the future.

(2) Guangdong: On February 20, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 120-50 yuan/mt, with an average discount of 85 yuan/mt, unchanged from the previous trading day. Overall, despite a large outflow of warehouse warrants, spot premiums remained flat compared to the previous day, but actual transactions were moderate.

(3) Imported Copper: On February 20, warehouse warrant prices ranged from $48 to $60/mt, QP March, with an average price down $1/mt from the previous trading day. B/L prices ranged from $50 to $62/mt, QP March, with an average price down $1/mt. EQ copper (CIF B/L) was quoted at $4-10/mt, QP March, with an average price down $1/mt. Quotes referenced cargoes arriving in late February and early March. Yesterday, the SHFE/LME price ratio for the SHFE copper 2503 contract was around -1,100 yuan/mt. LME 3M-Mar contango was at C$6.43/mt, and the March-April spread was around Backwardation $0.13/mt. Due to the sharp structural shift between LME March and April dates, the SHFE/LME price ratio experienced a rapid collapse. Suppliers mostly adopted a wait-and-see approach, with few offers for near-term cargoes. It is reported that domestic smelters have already started planning for exports.

(4) Secondary Copper: On February 20, secondary copper raw material prices rose by 100 yuan/mt MoM. Guangdong bare bright copper prices ranged from 70,800-71,000 yuan/mt, up 100 yuan/mt from the previous trading day. The price difference between primary metal and scrap was 1,814 yuan/mt, up 323 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,060 yuan/mt. According to an SMM survey, due to the continued tight supply of secondary copper raw materials, some secondary copper rod enterprises reported price competition for raw materials. Some enterprises currently have moderate raw material inventories, sufficient to ensure short-term normal production.

(5) Inventory: On February 20, LME copper cathode inventories decreased by 2,150 mt to 268,750 mt. On the same day, SHFE warrant inventories decreased by 4,869 mt to 152,463 mt.

Prices: Macro side, US initial jobless claims for the week ending February 15 slightly exceeded expectations, recording 219,000, higher than the forecast of 215,000. US Fed's Bostic stated that two interest rate cuts are still expected this year, but significant uncertainties remain. The US dollar index weakened significantly. Meanwhile, the US announced on Wednesday that new tariffs would be introduced within the next month or sooner. Trump announced that lumber tariffs might be announced on April 2. However, the US is currently negotiating a peace agreement with Russia, and lifting sanctions could be part of the deal. Trump also stated that the likelihood of reaching a trade agreement with China is high, potentially easing trade dispute concerns in the short term. With the US dollar index weakening significantly, copper prices remained at a strong level. Fundamentals side, the contango structure widened, reducing suppliers' willingness to sell spot cargoes. Meanwhile, as the export window opened, smelters began planning for exports, which is expected to support spot premiums in the future. As of Thursday, February 20, SMM's copper inventory in major regions nationwide increased by 7,300 mt from Monday to 357,600 mt, up 31,400 mt from last Thursday, and up 191,800 mt from pre-Chinese New Year levels. The inventory buildup in the first two weeks after the holiday exceeded last year's levels by 54,400 mt, marking the largest inventory buildup in the past seven years. Overall, with the US dollar index weakening significantly, copper prices are expected to gain support.

》Click to View SMM Metal Database

【The above information is based on market data collected and comprehensively evaluated by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make cautious decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】